1. Investment Philosophy

The Betteredge investment philosophy is built around a Preserve and Grow framework. There will be many opportunities to implement this in the investment environment that will increasingly favour selectivity and global diversification.

2. Short-Term Advice

Our overall view is cautious in the short-term, with ongoing uncertainties mainly relating to US domestic and foreign policymaking. This is starting to be reflected in slower US growth, lower US equity prices and the weaker US Dollar. US policymaking is also starting to impact on the rest of the world, which is likely to keep market volatility elevated and slow the European Central Bank and the Bank of England rate cutting cycles.

In this environment, we are advising our clients to hold high cash levels and to put cash to work very gradually. It’s the right time to hold overweight positions in quality bonds with short duration. For accounts which have low equity weightings, it is too early to raise those weightings aggressively. We like structures that take advantage of market volatility to build in principal protection and high coupons. Within asset classes, the environment is increasingly good for selectivity (by country, sector, and company), with visibility of potential returns being particularly important. Alpha-seeking is likely to be more rewarding than beta chasing.

3. Long-Term Advice

Our longer-term view is more constructive. Critical areas of US policymaking such as tariffs, will probably be clearer. This could help give renewed confidence to businesses as well as consumers and investors. There will be increasing non-US opportunities in all asset classes, partly supported by a weakening USD and by new growth drivers like defence in Europe and more aggressive policy easing in China. In that environment, the outlook should also improve for midcap stocks, emerging market debt and developed market high yield corporate bonds.

The Betteredge approach is to first assess the bank consensus for economic data, for market return forecasts, and for investment overweights and underweights. We then decide where the consensus is high conviction for good reasons and should be followed, and where we might differ. Finally, our team spend time on assessing the sustainability of the bank views and the best ways to access them. This month the main areas of interest have been global GDP growth and global EPS growth.

1. GDP Growth Forecasts

Global GDP growth is currently steady at around 3%. Even with parts of the world seeing slight growth pickups, overall, we agree with the OECD who recently noted “a softening of global prospects” and expect the consensus global growth forecast to fall to just below 3%.

There are more significant forecast changes at the country level. US GDP growth forecasts are moving lower to a new consensus of 1.7%. The Fed recently cut its own GDP growth forecast to 1.7%. The level of US economic policy uncertainty is higher than it has been for five years. Discretionary consumption is weakening as tariffs are expected to push up petrol and new home prices. At the same time the Fed raised their inflation forecast to 2.7% and are keeping rates steady for now. With steadier policymaking as the year progresses, we’d agree with the consensus that there should be support from two Fed rates cuts over the rest of the year which should lessen the likelihood of a much sharper growth slowdown.

Chinese GDP growth forecasts are rising off depressed levels, and this trend could be sustained with more aggressive policy support. The upper end of the forecast range is now just over 5% which is also the level that policy is targeting.

2. EPS Growth Forecasts

Typically, EPS growth forecasts correlate reasonably closely with GDP growth. However, the clearest current consensus EPS growth trend is the pickup in non-US EPS growth off depressed levels. In Europe for example, the expected average 3% EPS growth for this year is expected to be followed by 9% next year. The trend of US downward revision forecasts appears to be easing. The upcoming US tariff confirmations on 2nd April and company responses to that will be very important and the next company earnings season will give more vital guidance than normal. We expect the earnings outlook will become increasingly disparate, with differences between countries, sectors and companies. This is why we believe that careful selectivity is becoming increasingly important.

1. Equities

Within equities, the Betteredge view is that there will be more rotation within the US market while the overall market is likely to consolidate in a wide range with high volatility over the coming months. Critical to this view are early signs that the negative US earnings revision cycle is stabilizing, while the US technology sector has had a sizeable de-rating. US industrials should benefit later this year from Trump’s focus on generating a strong manufacturing revival and the US banks still look inexpensive even after better stock performance so far this year.

Non-US markets are seeing inflows from very light positioning last year. While the non-US markets are relatively attractively valued even after outperforming so far this year, we do not advise chasing but rather accumulating if the data supporting sustained recoveries keeps improving. In Europe, we are particularly focused on the potential German locomotive, as the new leader Merz has released the debt brake and is looking for a $600 billion infrastructure and defence spending boost which is expected to boost Germany’s GDP growth by 1% annually over the next decade. Emphasizing the significance of the announcement, the 10-year German Bund yield has risen by 25 bps to 2.8%. In China, we are encouraged not only by more concerted policy easy, but also by improving government support for key industries and companies.

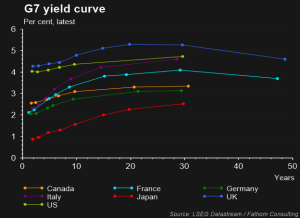

2. Fixed Income

Within fixed income, it’s a very good time to lock in decent yields in short-dated bonds which offer higher returns than cash. While developed market central banks are currently on hold as they await to assess the US tariff impact on inflation, we expect the downward rate trajectory to resume towards the middle of this year. As recently summarized by the Bank of England Governor Bailey: “There’s a lot of economic uncertainty at the moment. We still think that intertest rates are on a gradually declining path.” At this stage we don’t anticipate sharply higher long bond yields, nevertheless given the tariff uncertainty and ongoing supply pressures, it a something we are monitoring closely.

Our preference includes developed market sovereigns, where we note the rising debt sustainability concerns in several developed markets including the US, however, don’t see short-term signs of falling auction appetite nor ‘bond vigilante’ pressures. We also favor investment-grade corporate bonds despite tight spreads, because on a selective basis there are many quality issuers with strong cashflows. With both corporate high yield and emerging market bonds, there are selective opportunities with above-average yields, however given the uncertain macro backdrop in the short-term these are only advised for more aggressive portfolios.

3. Alternatives

We advise steadily increasing alternative weightings. In private equity the pressures of 2023-24 are easing as rates have fallen. Exits are a little easier and the operating environments are a little better. In private credit there are attractive selective low-teens yields, and the rapid recent sector growth is not a short-term concern. Within the hedge fund universe it’s an opportune time for macro strategies, and for equity long-short strategies, particularly those with active styles.

1. Non-US Equities Recovering

The US stock weighting is 66% in the global MSCI index, up from 42% in 2009, partly justified by better US returns on equity and US strong earnings growth over the last decade. We expect that this 66% will gradually decline. Foreigners now hold 30% of the US market and we expect this to gradually decline in the months ahead. A recent Bank of America survey showed the biggest ever swing in sentiment among global fund managers, with a net quarter now underweight US stocks. The same survey noted allocations to European markets have reached their highest in more than three years.

Outside of the US, markets only rose 6-7.5% last year however are outperforming the US so far this year. Even as non-US markets have started the year well and are now slightly more expensive that they were, they are still in aggregate 50% cheaper than US equities. The slight shift in relative GDP growth momentum, lower in the US and higher outside of the US, should give some fundamental support to the gradual ending of the ‘US exceptionalism’ market driver.

The China market does not need to be chased. While there are early signs of a GDP growth pickup, it is not yet clear that the progress with the China tech sector can sustainably turn the economy which remains held back by the weak property sector and concerns that a new US trade war is brewing. In addition, scepticism amongst investors is still high, which means that there will be profit-taking into rallies. It seems sensible to buy for the long-term when the new policy direction is certain and having impact, even if getting that certainty means buying in at slightly higher levels. What remains clear is that the China market is both cheap and investable – with a valuation half that of the US S&P Index, more than 250 companies with market capitalizations over $1bn, and an average free cashflow yield of more than 10%.

European underperformance has been very pronounced for many years and the valuation discount to the US is historically wide at 35%, and the Stoxx 600 index trades at only 14x. That said the 9% rally so far this year may not be sustained as investors have been disappointed before by disappointing nominal GDP growth. We will have a keen focus on whether European EPS growth meets expectations, which is currently forecast to rise from an average 3% this year to 9% next year.

Emerging markets have been resilient as the US market has weakened this year, which has seldom happened historically when the US market has been weak. Within the emerging markets, the Indian and ASEAN economic and market upturns could be more sustainable than in previous cycles. This is because their risk premia should keep falling as their institutional and regulatory frameworks improve, and as better market breadth and liquidity encourages long-term institutional money to markets that have to-date been dominated by retail flows.

2. US Technology Stocks Weakening

US tech companies will keep growing strongly, but at a slower pace than previously. The recent market consolidation in the sector is unlikely to result in a tech bear market as the business models and balance sheets are robust for the leaders, however there is not likely to be an immediate sustainable rebound. The US market's MAG-7 leaders are not likely to re-rate back to previous levels, and there are now also clearer differences in their operating performances.

There are likely to be more flows into privately held tech companies. In addition, we expect more rotation within the US market, to sectors like industrials and banks, with stock returns driven by earnings growth. Finally, there are now many non-MAG7 tech companies that are starting to benefit from AI. Specifically, there are companies that are making efficiency gains by investing in AI, robotics and automation technologies, and there are also sectors like healthcare and finance which are increasingly using technology to enhance decision-making and operational efficiency.

3. High Quality Bonds Look Attractive

While our positive views on high quality bonds are not new and the sector has had sustained strong price performance, there is further to go. Quality bonds should be overweighted in medium-risk portfolios where their expected total returns are above cash rates. In addition, as the cycle extends, we believe that portfolios should be starting to reach for yield by allocating to lower quality bonds. There are selective opportunities in going down capital structures within investment grade corporates. For more aggressive portfolios we advise selectively buying high yield corporate bonds of companies who have refinanced and pushed out their maturity walls, and EMD sovereigns and quasi-sovereigns.

Within the investment grade portion of portfolios, there is a growing case to diversify slightly into European bonds. The fiscal risks in both the US and Europe are not immediate concerns likely to pressure spreads further.

4. Global Trade War Escalating

The overall macroeconomic impact will take a few more months to become clearer, with key variables to monitor being the potential negative impacts on consumer sentiment and on business investment. What is becoming clearer is the likely assertive responses to US tariffs, even as those responses could have some negative impact for those countries, as recently noted by ECB president Lagarde “in the near term, EU retaliatory measures could lift inflation by around half a percentage point.”

There could be tactical opportunities around tariffs at a sector level, for example with the dislocation and relocations of some supply chains, however it is best to wait for clarity. Finally, while Trump’s ‘reciprocal’ approach so far arguably violates WTO laws and the MFN (Most Favoured Nation) principal, there has been little judicial pushback. If this changes then consumers, businesses and markets will be very challenged to price in the eventual trade outcomes, which would point towards more uncertainty and market volatility.

5. US Dollar Weakening

The trade-weighted USD is down 4% so far this year. This is the beginning of the end of the sustained period of trade-weighted USD strength. However, a USD collapse is not expected anytime soon and at present it is not easy to make strong sustainable bull cases for other major currencies. A key factor is gradually lowering confidence in the USD due to the growing uncertainty regarding USD domestic and foreign policies and well as the gradual undermining of the US institutional framework. This is starting to be reflected in the US “Trump Trades” losing momentum, which is weighing on flows supporting the USD.

6. Gold Rising

There is high gold momentum, reflected in the rapidly expanding gold stockpile in New York as banks and traders have rushed to move gold out of London since the US election. It is likely that bank forecasts will keep ratcheting higher this year. A key driver could be uncertainty relating to US policy, prompting more concerns about US Treasuries and the USD playing their traditional ‘safe haven’ roles. So gold is becoming the new “Trump Trade”.